The latest data from Cotality (formerly RPData) confirms what many investors are starting to sense: dwelling values are rising again in Melbourne and Sydney — and in some cities, the momentum is building fast.

Auction clearance rates across the capitals hit 71.6% last week, their highest level since June 2023, and national dwelling values rose 0.8% over the past 28 days. That’s a strong aggregate result, especially considering we’re still early in the rate-cutting cycle. According to Cotality’s latest chart pack, Australia’s total housing stock is now valued at a staggering $11.7 trillion, spread across 11.3 million dwellings — averaging just over $1 million per property.

But beneath the headline growth lies a more complex story — and one that highlights the importance of expert guidance.

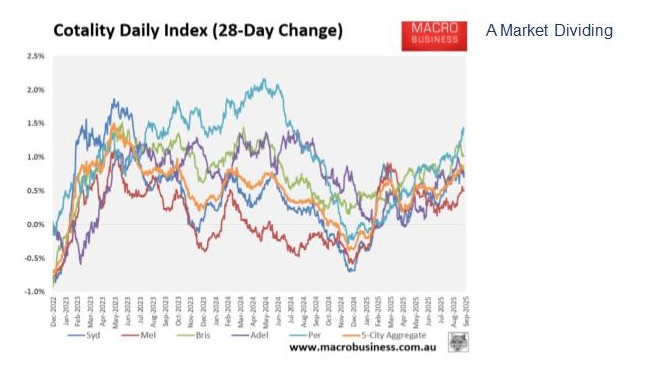

The chart below shows a widening performance gap between capital cities. Perth leads the charge, with prices continuing to surge off a low base, supported by strong mining activity and affordability. Melbourne, after years of flatlining, is now one of the best performers — with renewed buyer confidence, huge interstate investor appetite resulting in price movement since August.

Sydney is growing steadily, though more muted — many of its inner-ring markets are now brushing up against affordability limits while the outer west is under huge demand.

In contrast, Brisbane and Adelaide are starting to show signs of slowdown. While prices are still rising, the trend is flattening. After very strong runs since 2020, these markets may be entering a stabilisation phase — not dissimilar to what we’ve seen in Melbourne in recent years.

It’s worth noting that we’re only partway through the interest rate cycle. Even if the RBA slows its pace, Cotality’s modelling shows we’re still around two-thirds of the way through a typical rate-cutting upswing — which means further growth is likely throughout 2025 and into 2026.

Add to this the government’s new 5% deposit guarantee scheme, launching 1 October, which is expected to drive prices up by 3.5% to 6.6% over the following year (according to Lateral Economics). With increased borrowing capacity and competition from first-home buyers, the market could see a further uplift in activity and values — especially at the entry level.

So What Does This Mean for Investors?

The Value of Advice

This is exactly where professional support adds value. At 1Group, our job is to help clients cut through the noise, assess risk properly, and identify properties with genuine long-term upside.

It’s not about buying now for the sake of it — it’s about buying the right asset in the right pocket, backed by data and strategy.

If you're planning your next acquisition, let's talk about how to make it count.