The residential property market is not collapsing. It is changing.

After a long period where sellers held most of the power, buyers are finally starting to regain some leverage. That shift is unsettling for some, particularly after years of strong growth, rising rents and limited supply. But for disciplined buyers, this is not a reason to panic. It is an opportunity to be more selective.

The next phase of the market will not reward speculation or rushed decision-making. It will reward strategy, due diligence and the ability to separate genuine risk from short-term noise.

In The Intelligent Investor, Benjamin Graham describes “Mr Market” as a character who swings between irrational optimism and deep pessimism. One day he is confident and enthusiastic; the next he is fearful and depressed.

Residential property sentiment often behaves in a similar way.

Not long ago, the market was being driven by strong employment, population growth, rising rents, inflation, construction cost increases and limited housing supply. These factors supported price growth and gave everyone confidence.

Now, much of that has been overshadowed by concerns around interest rates, affordability, lending conditions and proposed tax changes affecting investors.

The fundamentals have not disappeared, but the mood has clearly changed.

Rates matter, but they are not the whole story

Interest rates are important, and they have a direct impact on borrowing capacity, confidence and cash flow.

However, the current rate outlook does not suggest financial Armageddon.

CBA and ANZ are effectively on hold, predicting the current rate as the peak. NAB expects one further 25 basis point increase to 4.60% in August, while Westpac is forecasting two further increases in August and September before rates peak.

Even if rates moved another 0.50% higher to 4.85%, that would create pressure, but it would not automatically lead to a broad residential property collapse.

The market has already absorbed a significant amount of tightening. Buyers, lenders and vendors are adjusting, and many households have already recalibrated their expectations.

What could happen to prices?

Despite the negative sentiment, most major forecasts point to moderate outcomes rather than dramatic falls.

CBA expects prices to be around 3% lower than they otherwise would have been, while Westpac expects relatively flat growth across the major capitals in 2026.

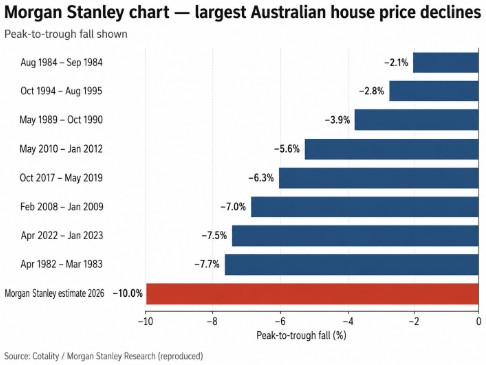

Morgan Stanley is more bearish and has warned that Australian home prices could fall by up to 10%, which would be significant. But even then, this would be a correction, not necessarily a collapse.

It is also important to remember that national can be misleading.

Property is not one market. It is thousands of smaller markets, each driven by its own mix of income levels, supply, demand, infrastructure, demographics, lifestyle appeal, school zones, employment access and housing stock.

Some areas will hold up well. Some will soften. Some will present genuine buying opportunities.

Long-term perspective matters

No one builds wealth by only focusing on the worst-case scenario.

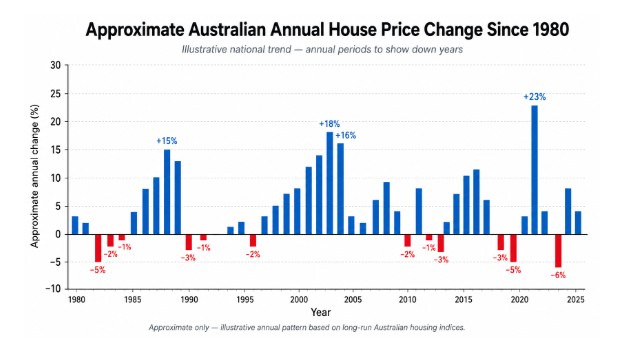

Since 1980, Australian residential property has moved through recessions, rate cycles, credit restrictions, global shocks, policy changes and repeated moments of market fear.

Yet over the long term, the trend has been overwhelmingly positive.

That does not mean every property is a good investment. It does not mean buyers should ignore risk. It does mean that fear alone is not a strategy.

The better approach is to understand where the risk sits, where the opportunity sits, and how to position yourself accordingly.

A more selective market

The most likely outcome from here is not a uniform national collapse.

Higher rates, affordability pressure and investor uncertainty will affect different locations and property types in different ways.

Quality assets in strong locations are likely to remain resilient, particularly where supply is limited and demand is supported by strong owner-occupier or tenant appeal. These more resilient markets will be opportunity as your usual 5-7 bidders may be 1 or 2.

Lower-quality assets, compromised locations, oversupplied markets and properties with weaker land value or limited scarcity may take longer to recover.

This is where the opportunity sits - A buyer’s market rewards preparation

A buyer’s market does not mean every property is cheap. It means buyers have more room to think, negotiate and apply proper due diligence.

For well-prepared buyers, this can be a very attractive environment.

That is where strategy matters.

Prescience is not a gift of humanity. No one can perfectly predict the next 12 months of the property market.

But good advice is not about pretending to know the future.

It is about reducing uncertainty, separating genuine risk from market noise, and helping buyers make informed decisions when others are hesitant.

A competent buyer’s agent does not need to predict the market perfectly. The role is to understand value, assess risk, identify opportunity and help clients act with discipline when the market changes.

The opportunity ahead

The market is not without risk.

Rates remain a factor. Policy changes may affect investor behaviour. Some property types will underperform. Some vendors will need time to adjust their expectations.

But a softer market is not something to fear.

For buyers with clear strategy, secure finance and a long-term view, it may be exactly the environment where better decisions can be made.

The key is not to panic.

The key is to be selective.